Insurance plays a fundamental role in making mental health therapy affordable and accessible for Californians struggling with anxiety, depression, or trauma. Yet many people face confusion about what their plans cover, how much they’ll pay, and which therapists they can see. Understanding how insurance impacts mental health care access helps you navigate coverage options, reduce costs, and connect with the right therapist for evidence-based treatment like EMDR or CBT.

Table of Contents

- The Connection Between Insurance And Mental Health Care Access

- Overview Of Mental Health Insurance Coverage In California

- Common Misconceptions About Insurance And Mental Health Access

- Financial Barriers Persist Despite Insurance Coverage

- Role Of Telehealth And Insurance In Expanding Access

- Strategies To Maximize Insurance Benefits For Mental Health Care

- Insurance Coverage For Evidence-Based Therapies Like EMDR And CBT

- Bridging Insurance Knowledge To Access Affordable Mental Health Care

- Explore Affordable Mental Health Therapy Options At Revive Health Therapy

Key Takeaways

| Point | Details |

|---|---|

| Insurance reduces therapy costs | Coverage lowers out-of-pocket expenses but co-pays and deductibles still apply. |

| California has strong mental health parity | Covered California and Medi-Cal mandate comprehensive mental health benefits equal to physical health. |

| Telehealth coverage is widespread | Over 85% of California plans cover telehealth mental health services. |

| Network and authorization limits persist | Prior authorization requirements and restricted provider networks create access barriers. |

| Strategic navigation improves affordability | Using HSAs, FSAs, and verifying in-network providers maximizes insurance benefits. |

The Connection Between Insurance and Mental Health Care Access

Insurance coverage stands as the primary financial gateway to mental health therapy in California. Without it, therapy costs can reach $150 to $250 per session, pricing out many individuals who need help with anxiety, depression, or trauma.

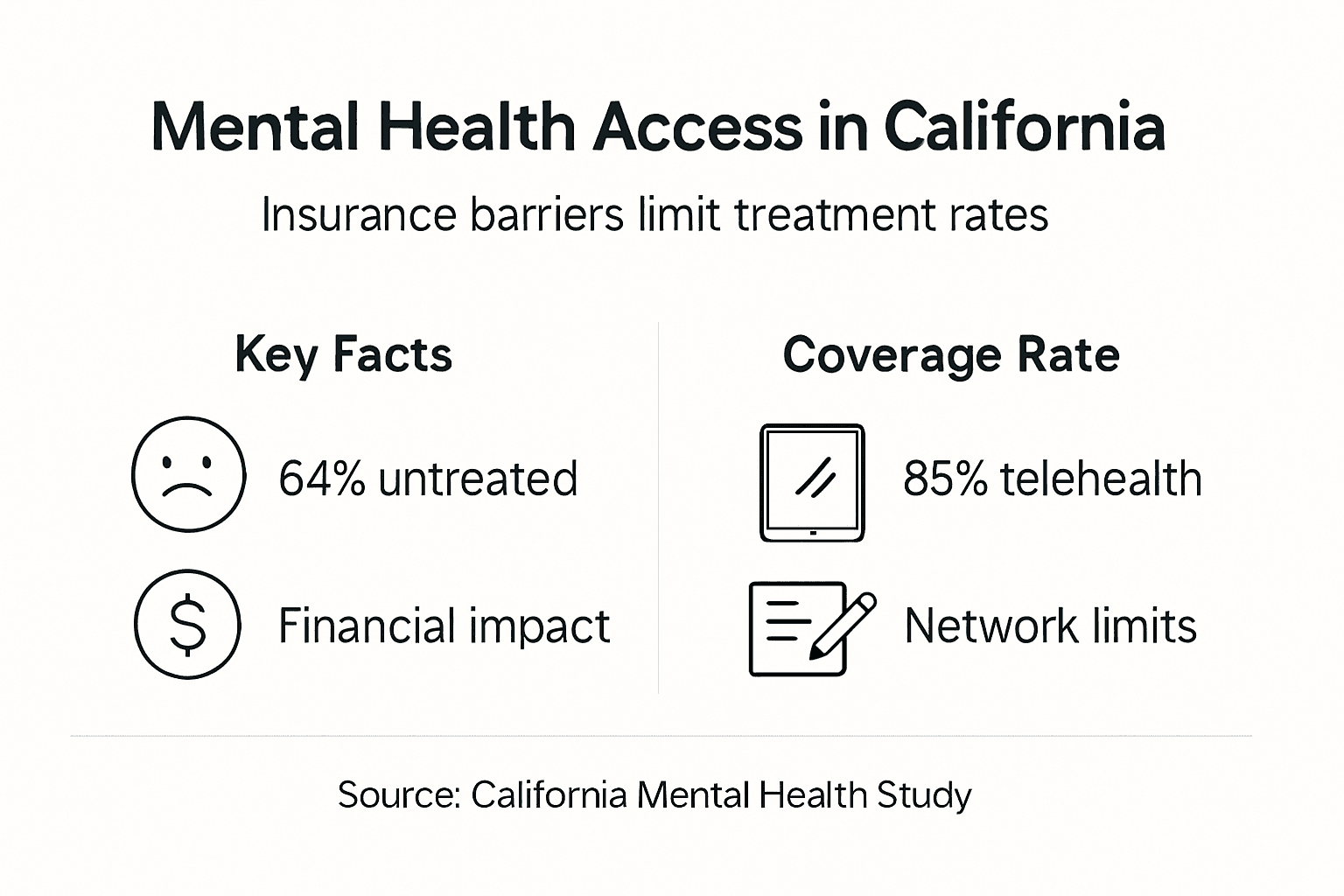

Nearly two-thirds of Californians with mental illness go untreated, largely due to insurance and cost barriers. When people can’t afford therapy, mental health conditions worsen. Anxiety escalates, depression deepens, and trauma remains unprocessed.

Insurance fundamentally changes this equation by:

- Reducing session fees to co-pay amounts instead of full price

- Covering evidence-based treatments like CBT and EMDR

- Expanding access to telehealth therapy across California

- Mandating mental health parity with physical health coverage

Key Statistic: Research shows that 64% of adults with mental illness in California do not receive treatment primarily due to mental health costs and insurance limitations.

Understanding how insurance works for mental health care represents the critical first step toward accessing affordable, effective therapy. The right coverage paired with informed navigation can mean the difference between getting help or continuing to struggle alone.

Overview of Mental Health Insurance Coverage in California

California offers several insurance pathways to mental health care, each with distinct coverage levels, costs, and provider networks. Knowing the differences helps you choose the best option for your situation and budget.

Covered California plans, sold through the state’s ACA marketplace, must include mental health and substance use disorder services equal to medical and surgical benefits. This mental health parity law ensures comprehensive coverage for therapy, psychiatric care, and crisis intervention.

Medi-Cal provides extensive mental health services for eligible low-income Californians with minimal or no cost-sharing. California insurance mental health coverage details show that Medi-Cal covers individual therapy, group therapy, medication management, and crisis services without deductibles for most enrollees.

Private insurance plans purchased outside the marketplace vary widely. Some offer robust mental health networks and low co-pays, while others impose high deductibles and limited provider choices.

| Insurance Type | Mental Health Coverage | Typical Costs | Provider Network Size |

|---|---|---|---|

| Covered California | Comprehensive parity coverage | $30-$75 co-pay per session | Medium to large |

| Medi-Cal | Extensive services | $0-$5 per session | Large, some access delays |

| Private Insurance | Varies by plan | $50-$100+ co-pay | Small to medium |

Understanding insurance impact on therapy access in California requires examining both coverage mandates and practical realities. Plans may cover therapy on paper but limit access through narrow networks or prior authorization hurdles.

Pro Tip: Before enrolling in any plan, verify its mental health provider network and confirm that therapists specializing in your needs (anxiety, trauma, depression) participate. Call the insurance company directly and ask for a current list of licensed therapists accepting new patients in your area.

Common Misconceptions About Insurance and Mental Health Access

Misunderstandings about insurance coverage create unnecessary barriers and frustration when seeking mental health therapy. Clarifying these myths helps you make better decisions and set realistic expectations.

Myth 1: All plans cover every therapy type including EMDR and CBT without restrictions.

Reality: While most California plans cover evidence-based therapies, coverage often requires prior authorization. 35% of insured patients mistakenly believe all therapy types are covered by their insurance plans without additional approval steps.

Myth 2: Having insurance guarantees easy, immediate access to a therapist.

Reality: Network limitations mean you can only see in-network providers without paying significantly more. Many therapists don’t accept insurance at all, limiting your choices. Authorization delays can postpone your first session by weeks.

Myth 3: Telehealth therapy is rarely covered by insurance.

Reality: California reformed telehealth coverage in 2023. Now over 85% of insurance plans cover telehealth mental health services at parity with in-person sessions. This expansion dramatically improves access for people in rural areas or with transportation challenges.

Recognizing these realities helps you navigate insurance misconceptions in therapy access more effectively. You’ll know to verify coverage details, check provider networks carefully, and understand authorization requirements before starting therapy.

Clearing up mental health insurance misconceptions prevents disappointment and guides you toward plans and therapists that truly meet your needs. Ask direct questions, read plan documents carefully, and don’t assume coverage without confirmation.

Financial Barriers Persist Despite Insurance Coverage

Even with insurance, financial obstacles can make consistent therapy difficult for many Californians seeking help with anxiety, depression, or trauma. Understanding these costs helps you budget realistically and choose the most affordable options.

Typical co-pays range from $50 to $75 per therapy session with insurance in California. For weekly therapy, that adds up to $200 to $300 monthly out of pocket. Over a year, you’re looking at $2,400 to $3,600 in co-pays alone.

Common hidden costs and access barriers include:

- Annual deductibles: You pay full session costs until meeting your deductible, which can range from $1,500 to $6,000.

- Out-of-network charges: Seeing a non-participating therapist often means paying 60% to 100% of session fees.

- Limited annual visit caps: Some plans restrict mental health visits to 20 or 30 sessions per year.

- Balance billing: Therapists may charge more than insurance reimburses, leaving you responsible for the difference.

- Medication costs: If therapy includes psychiatric medication, prescription co-pays add another expense layer.

Key Statistic: Studies show that cost-related barriers prevent 42% of insured individuals from continuing therapy long enough to see meaningful improvement in their mental health conditions.

Insurance provider networks create another financial pressure point. Narrow networks exclude many experienced trauma therapists, forcing you to choose between paying out-of-network rates or settling for a less specialized provider. Understanding financial barriers in mental health care empowers you to plan for these expenses.

Pro Tip: When comparing plans, calculate total annual therapy costs by multiplying weekly sessions by co-pay amounts, then adding your deductible. A plan with a higher premium but lower co-pay may cost less overall if you need consistent therapy. Also verify whether your preferred therapist accepts your insurance before enrolling.

Role of Telehealth and Insurance in Expanding Access

Telehealth has transformed mental health care access in California, particularly after insurance reforms made coverage mandatory for most plans. This shift benefits people facing geographic, mobility, or scheduling barriers to in-person therapy.

Over 85% of California insurance plans now cover telehealth mental health services, treating video sessions the same as office visits for reimbursement. This policy change removes a major obstacle that previously limited therapy options for many Californians.

“Telehealth mental health services expanded from 42% plan coverage in 2020 to over 85% coverage by 2023, with California leading insurance parity reforms that require equal reimbursement for virtual and in-person therapy sessions.” — California Telehealth Policy Landscape Report

Telehealth benefits for therapy access include:

- Geographic flexibility: Connect with specialized trauma or EMDR therapists anywhere in California, not just your local area.

- Transportation elimination: No commute time or costs, making therapy feasible for people with mobility challenges or unreliable transportation.

- Scheduling convenience: Evening and weekend appointments become more available when therapists serve clients across time zones.

- Privacy enhancement: Attend sessions from home, avoiding waiting rooms where you might encounter acquaintances.

- Continuity of care: Continue therapy if you move within California without finding a new provider.

Insurance reimbursement reforms strengthened telehealth mental health coverage California options by requiring plans to pay therapists the same rates whether sessions happen via video or in person. This financial parity encourages more therapists to offer telehealth, expanding your choices.

For people in rural California counties with few local mental health providers, california telehealth mental health coverage represents a genuine access breakthrough. You can now work with therapists specializing in anxiety, depression, or trauma treatment regardless of where you live.

Strategies to Maximize Insurance Benefits for Mental Health Care

Navigating insurance complexity requires strategic thinking, but specific tactics can significantly reduce your therapy costs and improve access to quality mental health care.

-

Access Employee Assistance Programs (EAPs) first: Many employers offer 3 to 8 free therapy sessions through EAPs before your insurance deductible applies. Use these sessions to start treatment immediately without upfront costs.

-

Leverage Health Savings Accounts (HSAs) and Flexible Spending Accounts (FSAs): Pay therapy co-pays and deductibles with pre-tax dollars, reducing your net cost by 20% to 35% depending on your tax bracket.

-

Verify in-network status before scheduling: Always confirm that your therapist participates in your specific insurance plan. Don’t rely on online directories, which are often outdated. Call both the therapist’s office and your insurance company to verify.

-

Understand prior authorization requirements upfront: Ask your insurance company which therapy types need pre-approval. Request authorization before your first session to avoid claim denials and unexpected bills.

-

Document all communications: Keep records of authorization numbers, representative names, and coverage confirmations. This documentation proves invaluable if claims are denied or disputed.

-

Request detailed Explanation of Benefits (EOB) statements: Review each EOB to catch billing errors early. Insurance companies make mistakes that can cost you hundreds if left uncorrected.

Strategically using these approaches to maximize insurance benefits for therapy can cut your out-of-pocket costs substantially while ensuring access to quality evidence-based treatment.

Pro Tip: If your insurance denies a therapy claim, file an appeal immediately. Many denials get overturned on appeal, especially for evidence-based treatments like CBT and EMDR. Also ask therapists about sliding-scale fees alongside insurance, combining both approaches can further reduce costs for those with financial constraints.

Insurance Coverage for Evidence-Based Therapies like EMDR and CBT

Evidence-based therapies such as EMDR (Eye Movement Desensitization and Reprocessing) and CBT (Cognitive Behavioral Therapy) represent gold-standard treatments for anxiety, depression, and trauma. Understanding how insurance covers these specific modalities helps you access the most effective care.

Most California insurance plans cover both EMDR and CBT under mental health benefits because clinical research demonstrates their effectiveness. However, coverage doesn’t guarantee seamless access.

Key coverage considerations include:

- Prior authorization requirements: Many plans require pre-approval for EMDR specifically, adding 1 to 3 weeks before treatment can begin.

- Therapist credentialing: Only licensed therapists (LCSWs, LMFTs, PhDs, PsyDs) who are in-network can bill insurance for these services.

- Session limits: Some plans cap EMDR or specialized trauma therapy at fewer sessions than general therapy.

- Documentation demands: Insurance may require therapists to submit treatment plans and progress notes justifying continued EMDR or CBT sessions.

- Diagnosis requirements: Coverage typically requires a qualifying diagnosis like PTSD, major depression, or generalized anxiety disorder.

Therapist credentialing significantly impacts your options. A highly skilled EMDR therapist who isn’t credentialed with your insurance plan can’t bill sessions, forcing you to pay out of pocket or find an in-network alternative with less specialized training.

Understanding insurance coverage of EMDR and CBT helps you ask the right questions when selecting both insurance plans and therapists. Verify that plans cover your needed therapy type and that qualified providers participate in the network.

Navigating these complexities requires patience and persistence, but accessing evidence-based treatment for anxiety, depression, or trauma makes the effort worthwhile. The right therapy approach, delivered by a skilled therapist and supported by insurance coverage, creates the foundation for meaningful mental health improvement.

Bridging Insurance Knowledge to Access Affordable Mental Health Care

Insurance serves as an essential tool for reducing mental health therapy costs, but it doesn’t eliminate all barriers to care. Knowledge bridges the gap between having coverage and actually accessing affordable, effective treatment.

Understanding your plan’s specific details matters more than simply having insurance. Co-pays, deductibles, network restrictions, and authorization requirements all shape your real-world access and costs. Being informed about these factors lets you choose plans strategically and navigate coverage rules effectively.

Combining insurance benefits with other affordability options creates the most accessible pathway to care. Sliding-scale fees, HSAs, FSAs, and EAPs work alongside insurance to minimize out-of-pocket expenses. Telehealth coverage expands your provider choices beyond geographic limitations.

Informed patients successfully navigate California’s complex insurance landscape by asking detailed questions, verifying coverage before starting therapy, and persistently advocating for their mental health needs. This proactive approach turns insurance from a confusing obstacle into a genuine resource for accessing the anxiety, depression, and trauma treatment you need.

Explore Affordable Mental Health Therapy Options at Revive Health Therapy

Now that you understand how insurance impacts mental health care access, it’s time to connect with professional support that works with your coverage and budget.

Revive Health Therapy specializes in affordable mental health care for Californians dealing with anxiety, depression, and trauma. We accept insurance, offer sliding-scale fees, and provide both in-person sessions in Walnut Creek and Oakland plus telehealth mental health access throughout California. Our therapists use evidence-based approaches including EMDR, CBT, and mindfulness to deliver effective treatment tailored to your specific needs. Whether you’re navigating insurance benefits or exploring affordable therapy options, we’re here to help you access the mental health support you deserve. Learn more about how psychotherapy for anxiety can transform your wellbeing.

Frequently Asked Questions

What should I check before choosing an insurance plan for mental health in California?

Verify the plan’s mental health provider network size and confirm it includes therapists specializing in your needs (anxiety, trauma, depression). Check co-pay amounts, annual deductibles, and whether prior authorization is required for therapy. Also confirm telehealth coverage if you prefer or need virtual sessions.

How can I confirm if my therapist accepts my insurance plan?

Call the therapist’s office directly and provide your specific insurance plan name and member ID. Then contact your insurance company to verify the therapist is listed as an active in-network provider. Don’t rely solely on online directories, which are frequently outdated and inaccurate.

Are telehealth therapy sessions covered by most California insurance plans?

Yes, over 85% of California insurance plans now cover telehealth mental health services at the same rate as in-person sessions following 2023 parity reforms. This coverage includes video therapy for anxiety, depression, and trauma treatment. Always verify your specific plan’s telehealth benefits before scheduling virtual sessions.

What can I do if my insurance denies coverage for EMDR or CBT?

File a formal appeal with your insurance company immediately, as many denials are overturned upon review. Request that your therapist provide clinical documentation supporting the medical necessity of EMDR or CBT for your diagnosis. If the appeal fails, ask about alternative evidence-based treatments your plan does cover or negotiate a reduced self-pay rate with your therapist.

How do HSAs and FSAs help reduce therapy costs with insurance?

HSAs and FSAs let you pay therapy co-pays, deductibles, and out-of-pocket costs using pre-tax dollars, effectively reducing expenses by 20% to 35% depending on your tax bracket. You contribute to these accounts through payroll deductions before taxes are calculated, then use the funds for qualified medical expenses including mental health therapy.

Recommended

- Telehealth in Mental Health: Expanding Access in California – ReviveHealthTherapy

- What Is Telehealth Therapy? Flexible Care for Californians – ReviveHealthTherapy

- Insurance and Therapy: Impact on California Families – ReviveHealthTherapy

- Why Is Therapy Accessible for Californians Today – ReviveHealthTherapy